Blog: The Capital Stack

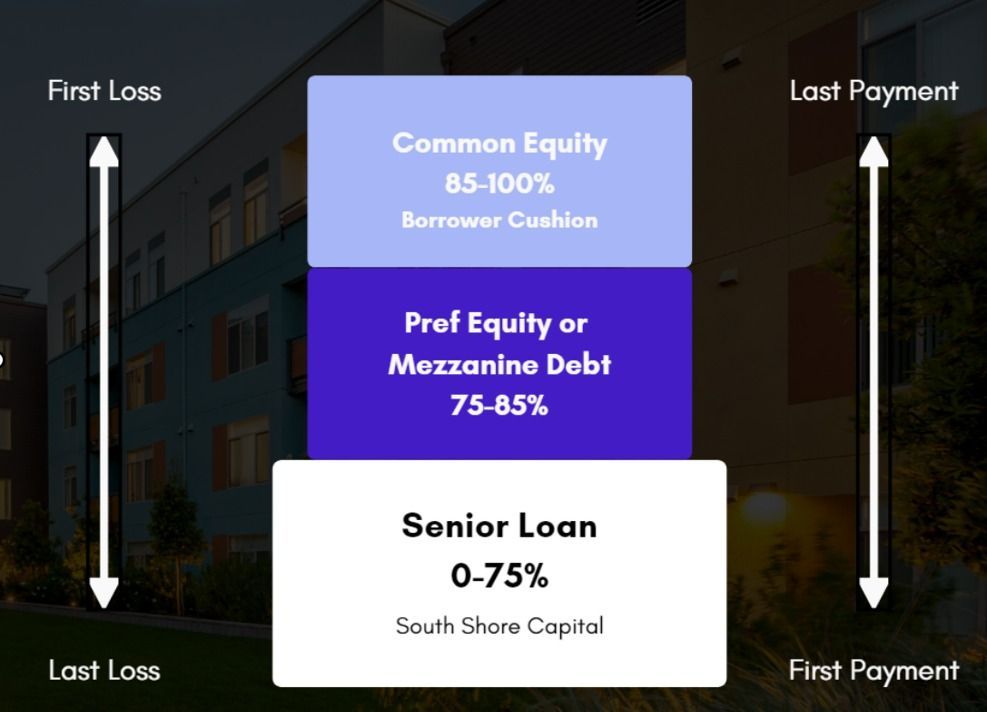

The capital stack refers to the funding tranches that make up the total value of a real estate asset. Equity and debt, along with subcategories of each, make up the composition of a capital stack.

Debt and equity partners look to invest their capital into a deal at an annual rate of return they accept to take on the risk of that investment. Risker projects command

Annual Return Requirement = A (position in the stack) + B (project risk profile)

Debt is first to earn cashflows and it takes a senior position in the stack. Debt is also last to lose their principal investment in the event that value erodes due to market forces.

Equity, on the other hand, is the last to earn cashflows and takes a first loss position in the stack. Equity is the first to lose their principal investment in the event that the equity provider must liquidate the asset. Usually, this occurs when the project's debt comes due while values are down; however, an asset could also be forced to sell at a loss due to perpetual operational mismanagement, leading to mortgage default in which the asset cannot meet its debt service obligation.

A subcategory of equity is commonly known as preferred equity. Preferred equity sits senior to common equity, but subordinate to debt. It commands a higher rate of return than debt and a lower rate of return than equity, being that it is sandwiched in between those sources. Pref equity typically has entity control or management rights triggered upon certain clauses, however, this requires underwriting by the senior lender. Pref can either be 'soft' or 'hard,' depending on the exact assumptions & stipulations made between the JV partners and debt partners. Typically with soft pref, the investor agrees to take on unlimited downside risk of potential reduced cashflows below expectations whereas hard pref requires DSCR and LTV basis stipulations on their investment.

For both equity and debt, investors aim to mimic the risk and return of their positions given the risk nature of the asset itself. Equity investors will demand higher annual returns for a distressed asset in an emerging, unproven area than they would a stabilized asset in an established, primary growth market.

Quick Links

Subscribe

Subscribe to receive the latest AEG articles about CRE investing, industry and market insights, and company updates.

invest@alphaequitygroup.com

Investment Disclaimers:

- Past performance is no guarantee of future results. No representation is made that the firm will or is likely to achieve its objectives or that any investor will or is likely to achieve results comparable to those shown or will make any profit at all or will be able to avoid incurring substantial losses.

- In many of the firm’s offerings, investors must be “accredited investors” as defined in regulation d under the securities act. In such cases, investors will be required to submit verification of their accredited investor status through the verify investor platform. The firm will not accept any investments from investors who are unable to submit verification of accredited investor status for relevant offerings. The principles, in their sole discretion, may decline to accept the subscriptions of, and admit, any investor as a member for any or no reason.

© 2024 Alpha Equity Group, LLC