Fed Balance Sheet Talk

Fed's Balance Sheet - Why It Matters

Simply put, the Fed’s Balance Sheet materially impacts the CRE sector by influencing global capital flows, which drive the supply and demand for tangible assets such as real estate. Surprisingly, when you look at history, the flow of funds influences cap rates more than interest rates do. In other words, the amount of currency in circulation chasing real assets has a greater impact on pricing of those assets than the cost of debt. But, that is an article for another time.

The Feds balance sheet serves as a tool to stimulate or restrict economic growth in the market by increasing or decreasing liquidity and consequently, borrowing. On the asset side of the balance sheet, the Fed holds treasuries, mortgage-backed securities, and assets under a variety of lending facilities like the discount window and repo facility. Fed liabilities include bank reserves on deposit, currency in circulation, and reverse repurchase agreements.

Inflation is the expansion of the money supply. When the Fed wants to increase the amount of currency in circulation, it engages in quantitative easing whereby it purchases treasuries and assets on the market. This act elevates prices and drives yields down. When it wants to decrease liquidity or currency in circulation, it sells treasuries and assets to the market, pushing prices down and yields up.

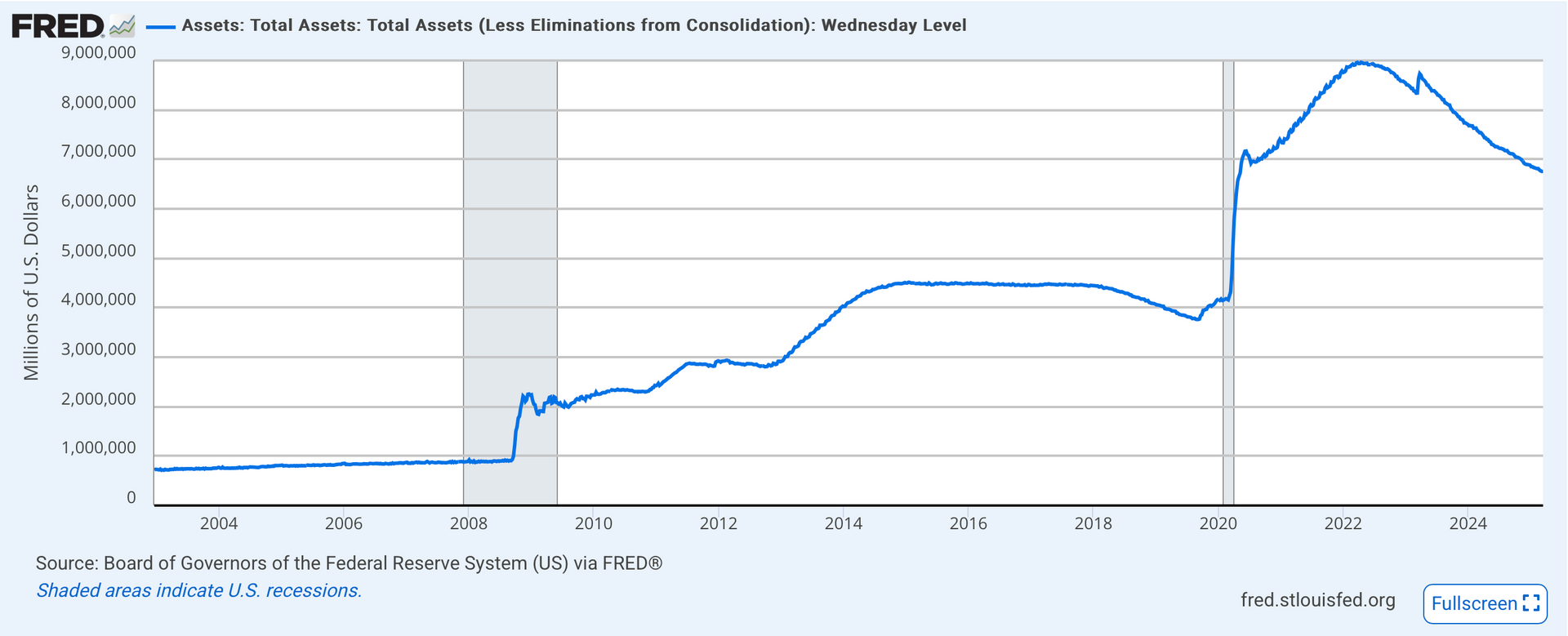

After the 2008 financial crisis, the Fed, and other central banks around the world, rushed to stabilize the save the financial system by purchasing underwater securities and assets from the market, flushing cash back out and stimulating the economy. By the end of QE round 1 in March of 2010, the Fed had purchased 1.725 trillion worth of financial assets, and they continued to engage in more rounds of QE.

In 2020, 20% of all US dollars in circulation were printed to stimulate the economy in the wake of the pandemic. The short-term rate, another tool the Fed can use to influence market participation, dropped to virtually 0%. Fast forward to March of 2022 and US inflation peaked at a 41 year high of 8.5%. But how? Fundamental economics. If there are too many dollars chasing a fixed amount of goods and resources, prices go up. When the Fed buys assets and/or issues new debt (creates currency), these dollars eventually make their way into risky assets. The lower the risk-free yields are, the greater the appeal to chase higher returns in risky assets like real estate and stocks. In a nutshell, that explains the inherent tie between the Fed’s balance sheet and asset prices.

Starting in April this year, the FOMC (Federal Open Market Committee) will be reducing the number of treasuries that will be rolling off the Fed’s balance sheet by roughly 80%. Instead of treasuries rolling off and being absorbed by the private market, who demands higher yields, the Fed will reinvest proceeds back into new security purchases, elevating prices and suppressing longer-term yields more than the market would naturally allow.

As the value of debt continues to come into question by the supply and demand of debt, investors will seek to re-balance their portfolios accordingly to mitigate ongoing volatility.

Tangible, fixed supply real estate remains a compelling investment option in the face of uncertain economic, inflation concerns, and policy conditions. Specifically, residential real estate, a non-discretionary asset that everyone needs to survive, will continue to command interest. By keeping an eye on the Fed’s balance sheet and forward-looking indicators, we can make better risk-adjusted investment decisions. The more dollars there are chasing inflation hedged assets, the higher valuations should be, regardless of negative leverage.

Quick Links

Subscribe

Subscribe to receive the latest AEG articles about CRE investing, industry and market insights, and company updates.

invest@alphaequitygroup.com

Investment Disclaimers:

- Past performance is no guarantee of future results. No representation is made that the firm will or is likely to achieve its objectives or that any investor will or is likely to achieve results comparable to those shown or will make any profit at all or will be able to avoid incurring substantial losses.

- In many of the firm’s offerings, investors must be “accredited investors” as defined in regulation d under the securities act. In such cases, investors will be required to submit verification of their accredited investor status through the verify investor platform. The firm will not accept any investments from investors who are unable to submit verification of accredited investor status for relevant offerings. The principles, in their sole discretion, may decline to accept the subscriptions of, and admit, any investor as a member for any or no reason.

© 2024 Alpha Equity Group, LLC