Blog Layout

Blog: What is an accredited investor?

An accredited investor has either a net worth of $1mil, not including their primary residence, OR an annual income of $200,000 (or $300,000 if married) for the last two years and you have a reasonable expectation that it will continue.

Feel free to contact us if you have further questions regarding whether or not you are an accredited investor.

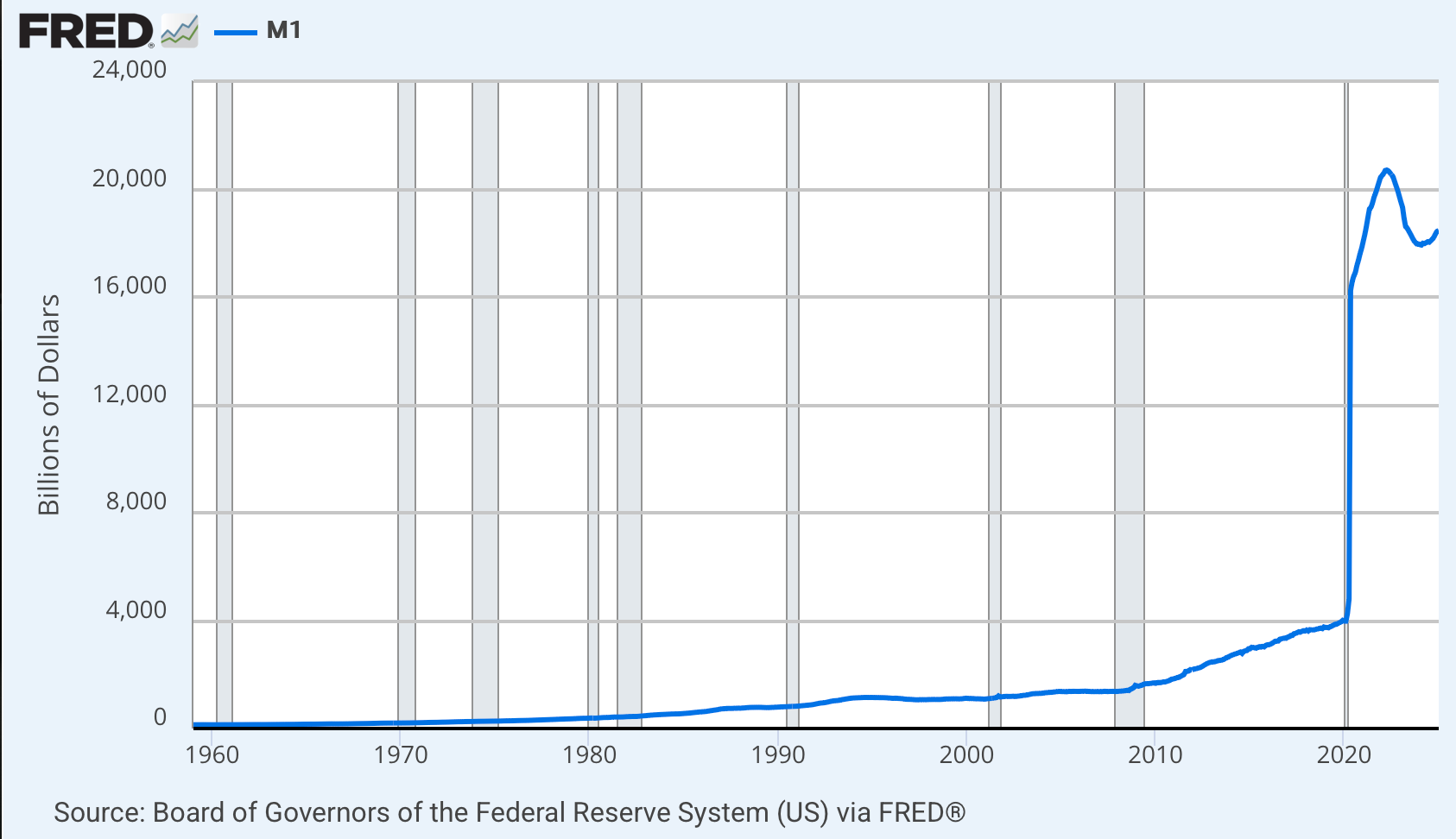

Fed's Balance Sheet - Why It Matters

Impact of Tariffs on CRE

The fundamental need for housing is universal—everyone requires a roof over their head. In the United States, however, we are facing a significant shortage of housing. According to the National Multifamily Housing Council, an additional 4.3 million units will be needed by 2035 to meet growing demand. Much of this demand is driven by migration to expanding lower cost cities and away from high tax, high cost metros, a trend accelerated by the widespread adoption of remote work during the pandemic. This trend has reshaped the housing landscape, creating a compelling opportunity for investors. While there are numerous investment strategies available, each with its own set of risks, residential real estate stands out. Over the past three decades, multifamily rentals have consistently delivered the highest risk-adjusted returns in commercial real estate. Why? Because housing is an essential need, regardless of economic conditions. At AEG, we are strategically developing both for-sale and rental housing, allowing us to adapt our approach to changing market dynamics and maximize returns while mitigating risk. Here’s why we are confident in the strength of residential housing as an investment: Land is Finite: Unlike many other asset classes, land cannot be created or expanded. The supply is fixed, and the demand for housing continues to grow. In the foreseeable future, virtual spaces like the metaverse will not replace the fundamental human need for physical shelter. Residential Housing is Non-Discretionary, and It's Supported by Government Liquidity: Housing is the only non-discretionary asset class. If it weren’t, we would see similar government support for other sectors like retail, office, or industrial real estate, but we don't. The federal government provides liquidity to the multifamily housing market because it is a fundamental need. This support drives down the weighted average cost of capital (WACC), making housing assets attractive to investors. This consistent access to capital compresses cap rates, creating a floor on the market (to an extent), fueling long-term growth and demand from investors big and small. Rents Tract with Inflation, and It is Rare to See Negative National Rent Growth: Rents reset every year as cost increases are passed off to tenants via annual lease contract resets. Since the beginning of recorded history, national rents have only gone negative year over year three times: the Spanish flu of 1918, the Great Financial Crisis, and during the Covid-19 pandemic. While yearly gains in rental cashflow streams will not make you wealthy, they are without a doubt very stable cashflows, historically speaking. There is no similar liquidity for for-sale housing, but its non-discretionary nature still gives it a strong investment profile. In growth markets like South Carolina's tertiary cities, the influx of new residents is fueling demand across all price points, further strengthening the residential sector. We believe in our residential investment thesis for both macro and local fundamental reasons. If interest rates remain high, new construction will slow even further. Meanwhile, homes in desirable locations will remain in high demand as many homeowners—especially those with low-rate mortgages—are unlikely to sell. According to the latest third-quarter data from the FHFA, 73.3% of U.S. mortgage borrowers now have an interest rate below 5.0%, a decline of 12.2 percentage points since Q1 2022. This significant shift in mortgage rates creates a unique dynamic: many homeowners are effectively "locked in" to their current homes, preventing them from moving and creating a looser supply in the for-sale market. As a result, home prices are expected to remain elevated in high-demand areas. While values may remain relatively flat in real terms over the next few years, on a nominal basis, they are expected to rise, particularly in growing markets. If interest rates decrease or economic growth drives up rental demand, build-for-rent communities could become more viable. However, they are not yet penciling out as attractive investments because growth has stalled - but, that is about to reverse. Thanks to our strategy and access to land—often without burdening our balance sheet or stretching our resources—we are able to remain nimble and pivot towards the most attractive risk-adjusted yields. As we navigate an uncertain economic environment, several factors support the ongoing strength of the residential housing market: slow housing starts, higher interest rates, and a large percentage of homeowners sitting on mortgages with sub-4% rates. These dynamics, along with strong demand in high-growth areas, reinforce our belief that residential real estate will remain a compelling investment in the years to come. At AEG, our focus is on developing attainable, high-quality housing, from custom spec homes, to mini-farm tracts, to higher density townhome projects. This flexibility allows us to serve a wide range of income levels and tailor our strategy to market conditions. With a commitment to quality finishes and high end products, we appeal to buyers regardless of economic conditions, providing us with a tighter, more predictable cash conversion and days on market cycle, unlike some of our competitors. By seeking out individually parceled deals, we reduce overall risk and remain agile in our decision-making.

Quick Links

Subscribe

Subscribe to receive the latest AEG articles about CRE investing, industry and market insights, and company updates.

invest@alphaequitygroup.com

Investment Disclaimers:

- Past performance is no guarantee of future results. No representation is made that the firm will or is likely to achieve its objectives or that any investor will or is likely to achieve results comparable to those shown or will make any profit at all or will be able to avoid incurring substantial losses.

- In many of the firm’s offerings, investors must be “accredited investors” as defined in regulation d under the securities act. In such cases, investors will be required to submit verification of their accredited investor status through the verify investor platform. The firm will not accept any investments from investors who are unable to submit verification of accredited investor status for relevant offerings. The principles, in their sole discretion, may decline to accept the subscriptions of, and admit, any investor as a member for any or no reason.

© 2024 Alpha Equity Group, LLC